If you are considering buying or selling a business you might have wondered does the size of the business matter? It seems intuitive that larger businesses would be safer. But is that just perception and not reality? I recently embarked on a journey to find the answer. To ascertain whether the size of a business matters I studied the default rates of SBA 7(a) loans made between 2010-2019. This dataset included 545,751 businesses funded by banks nationwide using the SBA 7(a) loan program. Based upon the results of my study I noted that larger deals had significantly lower default rates.

Methodology

I calculated the default rates of businesses within three industries to determine if smaller business transactions within the industry failed more often than larger business transactions within the industry. I chose three unique industries restaurants, machine shops, and offices of certified public accountants. These three industries should be representative of three major sectors of the US economy: food service, manufacturing, and personal services. Within each industry I sorted the transactions based upon deal size. The sort ranges were deals less than $500,000, deals greater than $500,000 but less than $1,000,000, deals between $1,000,000 and $2,000,000 and deals greater than $2,000,000.

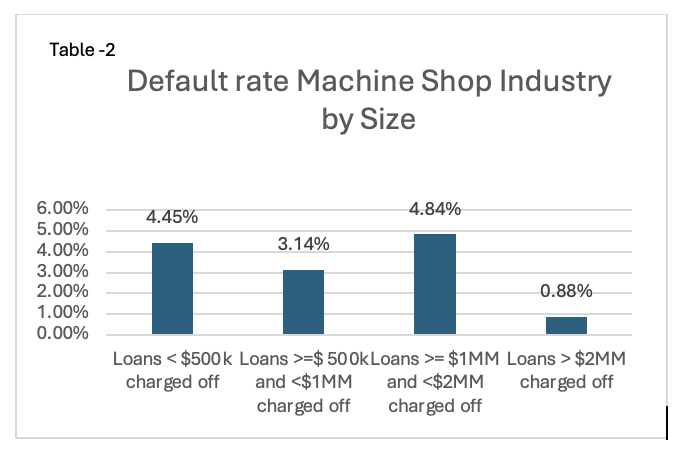

Within each industry a pattern was identified. The deals less than $500,000 had a higher default rate than the larger deals. This was consistent as deal size increased so that the largest deals had the lowest default rates. The only exception was machine shops, which inexplicably had a higher default rate for business transactions between $1,000,000 and $2,000,000. Otherwise the larger businesses within each stratum were more likely to succeed.

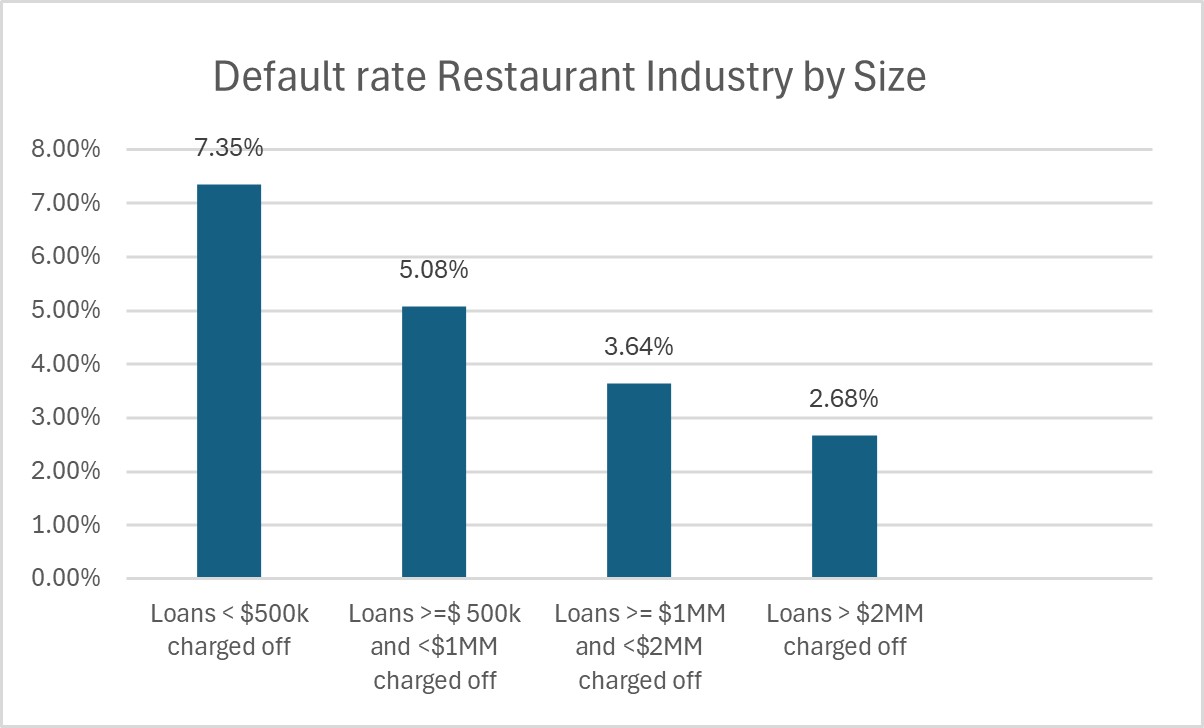

Restaurant Industry

The smallest business defaulted at a 7.35% clip versus a 2.68% default rate for the largest segment. Thus a transaction of a larger restaurant greater than $2,000,000 had a 97.32% success rate during the 10 year period of my study (2010-2019). This is a relatively healthy success rate for an industry that has a poor reputation for failure rates (table -1).

Machine Shop Industry

Similar to the restaurant industry the largest businesses within the machine shop industry were most likely to succeed. The success rate was over 99% for purchases of machines shops greater than $2,000,000. This was higher than the 95.55% success rate for the smallest transactions. There was one anomaly within this industry. Transactions between $1,000,000 and $2,000,000 had the highest default rate 4.84%. This was an aberration within this dataset (table – 2).

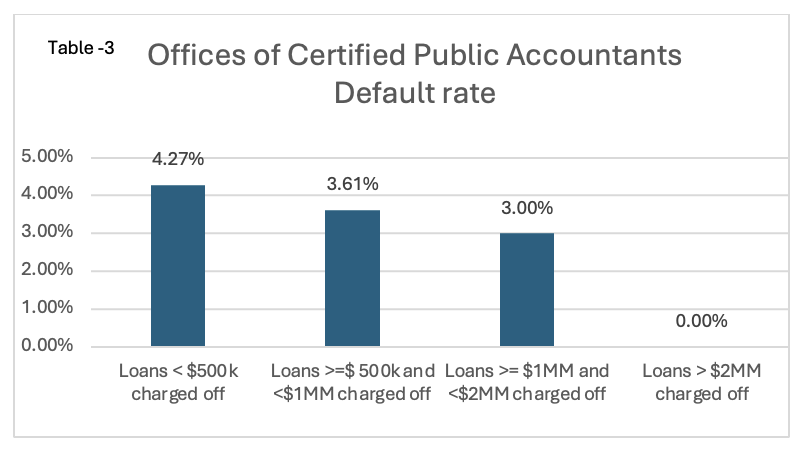

The chasm between small and large was even more evident within the accounting industry. The largest businesses had a 100% success rate or 0% default rate while the smallest businesses failed at 4.27%. The low default rate among all size transactions is a testament to the resilience of the accounting industry. Revenue is “sticky.” Most customers are required to obtain an accounting service on a monthly, quarterly, or annual basis by government reporting requirements e.g., IRS, State, or other regulatory body. It is not easy to transfer 50 employees’ payroll records from one accounting firm to another. Accounting is a boring but bodacious industry (table – 3).

Insights for Buyers and Sellers

This analysis provides us with empirical evidence that larger transactions are more likely to succeed than smaller deals. There are numerous reasons that can help explain this phenomenon. Larger businesses have greater cash flow and can weather downturns in the industry and economy better. Key employees at the larger businesses can likely operate the business for the buyer. Whereas the seller of many small businesses took sole responsibility of operations. The larger businesses typically have a larger customer base and would experience less impact from the loss of a few customers that can occur during the transition of a business to new ownership. Larger businesses are more likely to have a sustainable customer acquisition system.

Implications

This study shows the importance for prospective sellers to grow their businesses to a point where key employees can run the business apart from the seller. This will likely lead to increased cash flow, increased depth of management, decrease the reliance upon the owner, and increase the customer base. If an owner is ready to sell and does not have time to grow the business that is okay. The owner can still delegate as much as they can to key employees. For prospective buyers it is clear that a larger business is more likely to succeed during a transition of ownership. Purchase the largest business you can afford. If your budget only allows for a very small business purchase a business with a high quality cash flow i.e., a broad customer base, recurring or sticky revenue, and require that the owner/seller stay onboard for a lengthy training period.