In a previous article we discussed how net working capital depicts whether a business has enough liquid assets on hand i.e., current assets to pay for expenses that are coming due soon i.e., current liabilities. If a company has more current assets than current liabilities it indicates the company is liquid enough to handle short-term expenses and thus it is financially sound in the short term. But how do we determine how much working capital a company needs based upon how much time it takes to convert each sales dollar into cash and then pay expenses. To figure how much working capital a business needs we must examine the business operating cycle. For this topic we turn our attention to the cash conversion cycle (CCC), also called the net operating cycle or cash cycle. It is a metric that expresses, in days, how long it takes a company to convert the cash spent on inventory (or labor for service companies) back into cash from selling its product or service.

The cash conversion cycle attempts to measure how long each net input dollar is tied up in the production and sales process before it gets converted into cash received. This metric considers how much time the company needs to sell its inventory, how much time it takes to collect receivables, and how much time it has to pay its bills.

The CCC is one of several quantitative measures that help evaluate the efficiency of a company’s operations and management. A trend of decreasing or steady CCC values over multiple periods is a good sign while rising ones should lead to more investigation and analysis based on the other factors. One should bear in mind that CCC applies only to sectors dependent on inventory management and related operations.1 But with a few tweaks the formula can be insightful within most sectors, even service sectors. For example by classifying wages (needed to provide a service) to the cost of goods the formula can be used for a professional service firm or other labor-intensive companies.

Since the CCC involves calculating the net aggregate time involved across the three stages of the cash conversion life cycle, we need to calculate the days sales outstanding or DSO, the days inventory outstanding or DSI, , and finally the days payable outstanding or DPO. The cash version formula is represented as:

CCC = DSO + DSI – DPO

DSO = Avg. Accounts

Receivable/Revenue X 365 Days

The first stage focuses on the current sales and represents how long it takes to collect the cash generated from the sales. The figure is calculated by using the days sales outstanding (DSO), which divides average accounts receivable by revenue per day. A lower value is preferred for DSO, which indicates that the company is able to collect capital in a short time, in turn enhancing its cash position.

The first stage focuses on the current sales and represents how long it takes to collect the cash generated from the sales. The figure is calculated by using the days sales outstanding (DSO), which divides average accounts receivable by revenue per day. A lower value is preferred for DSO, which indicates that the company is able to collect capital in a short time, in turn enhancing its cash position.

DSI = Avg. Inventory/COGS X 365 Days

The DSI (days sales of inventory) focuses on the existing inventory level and represents how long it will take for the business to sell its inventory. This figure is calculated by using the days inventory outstanding. A lower DSI is preferred, as it indicates that the company is making sales rapidly, implying better turnover for the business. is calculated based on the cost of goods sold (COGS), which represents the cost of acquiring or manufacturing the products or services that a company sells during a period.

The DSI (days sales of inventory) focuses on the existing inventory level and represents how long it will take for the business to sell its inventory. This figure is calculated by using the days inventory outstanding. A lower DSI is preferred, as it indicates that the company is making sales rapidly, implying better turnover for the business. is calculated based on the cost of goods sold (COGS), which represents the cost of acquiring or manufacturing the products or services that a company sells during a period.

DPO = Avg. Accounts Payable/COGS X 365

The third stage focuses on the current outstanding payable for the business. It takes into account the amount of money that the company owes its current suppliers for the inventory and goods its purchases, and it represents the period in which the company must pay off those obligations. This figure is calculated by using the days payable outstanding, which considers accounts payable. A higher DPO value is preferred. By maximizing this number, the company holds onto cash longer, thus increasing its investment potential.

The third stage focuses on the current outstanding payable for the business. It takes into account the amount of money that the company owes its current suppliers for the inventory and goods its purchases, and it represents the period in which the company must pay off those obligations. This figure is calculated by using the days payable outstanding, which considers accounts payable. A higher DPO value is preferred. By maximizing this number, the company holds onto cash longer, thus increasing its investment potential.

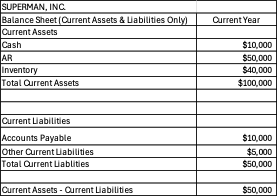

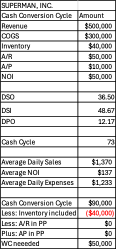

Probably the best way to understand this calculation is to see it. So, please examine the sample financial information below for Superman, Inc. In this example we will calculate the CCC for the company. Below are the relevant pieces from the company’s balance sheet and income statement. Following the CCC formula we find the DSO calculation returned 36.5 days, which represents the number of days it takes for the company to collect receivables. It took 48.67 days for the inventory to be sold, and the payables were paid in 12.17 days. Summing this up we get a CCC of 73 days (36.5 days + 48.67 days – 12.17 days).

Now we can utilize the CCC cycle to help us calculate the business working capital needs. We know from the CCC calculation that Superman, Inc. averages 73 days to convert invested cash on inventory back into cash from selling its product. Next, we calculate the amount of working capital needed to fund 73 days. Since average daily sales are $1,370 and average net operating income (NOI) is $137 average daily expenses are $1,233 ($1,370 – $137). If we spend $1,233 per day and our CCC is 73 days, we need $90,000 of working capital.

Now assume you were buying or selling Superman, Inc. and the deal includes inventory of $40,000 but no cash, receivables, or liabilities. How much cash would the buyer need to borrow or inject in order to operate the business under normal conditions? The answer is $50,000 ($90,000 – $40,000).