White Papers

In the early stages of the business life cycle you don’t have much time to think about selling your business, it can even seem premature. But after years of success it becomes obvious that you need a plan to help guide you and other stakeholders on what your ultimate desire is once you are ready to move on. This plan is called exit or succession planning. The first step of any good exit strategy is a business valuation.

Many folks purport to prepare valuations. In this article, you will learn the subtle and not so subtle differences between valuations and valuators. If you or someone you know needs to start an exit plan, the referenced article is a great place to begin.

The first step to selling your business is to obtain a business valuation. The subsequent steps are vital to help you eventually transfer ownership to your family, employees, or sell to a third party. You will need to build a team that will help you execute your plan. Your succession team will likely need to include a business transaction attorney, a competent business intermediary/broker, a trusted banker, and a knowledgeable investment advisor.

It is important that you start to plan sooner rather than later. By planning ahead you will give yourself margin for adjustment, and it will help you and your inner circle in the event you become incapacitated. A recent survey showed that only 34% of closely held businesses in America have a robust succession plan in place. Most businesses do not survive past the first generation but with a succession plan you can be in the minority of business owners who successfully build a lasting legacy for their family, employees, and community. I authored an article that will help ensure you are taking the right steps toward building a robust succession plan.

With rampant inflation and rising interest rates in the headlines folks are wondering how this will affect small business valuations. As you might expect there is an inverse relationship between rising interest rates and business value.

However, there is some good news too—rising interest rates do not appear to affect private business values as their publicly traded counterparts. This article will provide you with an overview of how inflation and rising interest rates affect private business value.

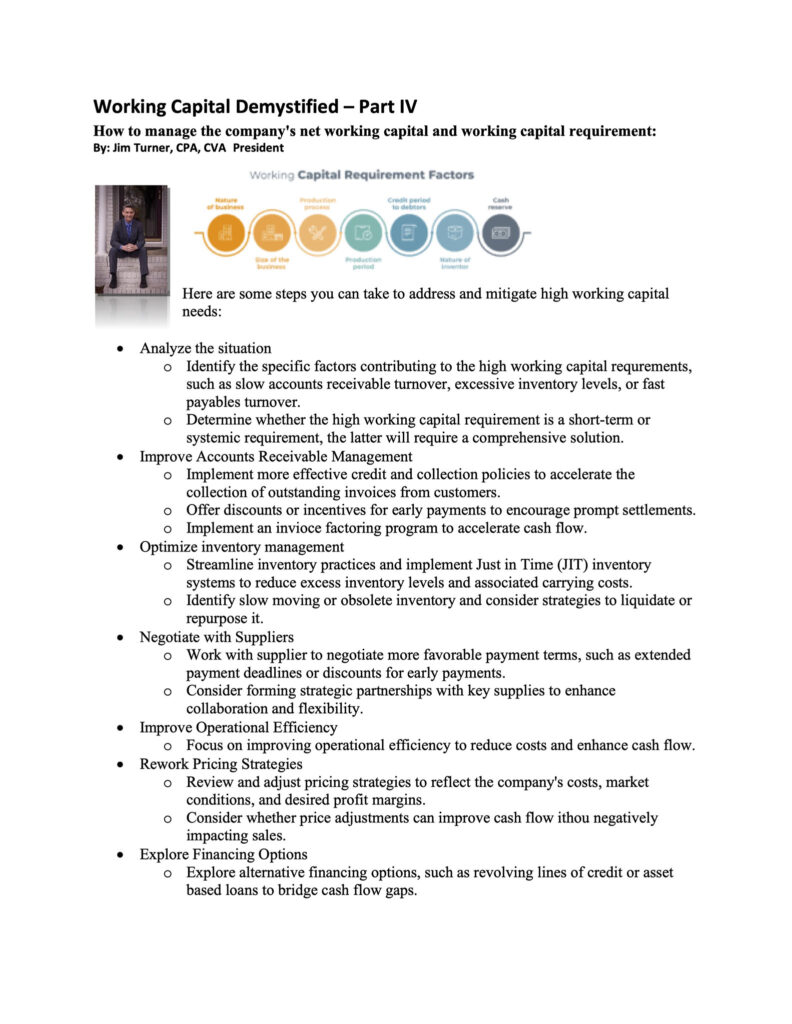

Working capital is often a puzzling topic to business owners and folks interested in buying or selling businesses. It is an important topic though as working capital is the life blood of a business. Too little working capital can literally been a death nail for a business. Too much working capital means the business is not efficiently utilizing its current assets.

The textbook definition of working capital is the net of current assets minus current liabilities. If you have positive working capital, it indicates the business is liquid and financially sound in the short run. The business appears to have the ability to pay the liabilities coming due within the next year with its current assets i.e., cash, receivables, and inventory. This article includes a sample balance sheet and the calculation of working capital for Superman, Inc.

Understanding the difference between net working capital versus working capital requirement is the crux of the second part of our series on working capital demystified. While net working capital depicts if a business has positive or negative working capital it does not tell us how much working capital the business needs.

The working capital requirement is one of the formulas we can utilize to calculate how much working capital a business needs to operate efficiently.

The cash conversion cycle attempts to measure how long each net input dollar is tied up in the production and sales process before it gets converted into cash received. This formula can be utilized to calculate how much working capital the business needs to operate efficiently. The formula for the Cash Conversion Cycle is Days Sales Outstanding “DSO” + Days Sales of Inventory Outstanding “DSI” – Days Payable Outstanding.

In this article we calculate the cash conversion cycle “CCC” for a sample company. This is a user-friendly way for the reader to gain a deeper understanding of the intricacies of the cash conversion cycle. As we show you precisely how to calculate each of the three inputs for the CCC. The information gleaned from calculating the CCC can help management run a business more efficiently and it can help the buyer and the seller during the negotiations of a business transaction to determine how much working capital the target needs to operate efficiently.

What are some steps a business owner can take to decrease its working capital needs? That question is tackled in this article. By consistently monitoring working capital management will be more likely to avert the inefficient use of working capital. There are several actions a business can take to mitigate having too much or too little working capital. Analyze the elements of working capital on a regular basis. If working capital requirements are growing management can analyze accounts receivable turnover, excess inventory, or fast payables turnover.

Management can improve accounts receivable collections by implementing effective credit and collections policies. Inventory can be streamlined by implementing Just In Time (JIT) inventory systems to reduce excess inventory. Another strategy is to negotiate better terms with suppliers. Systematic monitoring of the cash flow and working capital position will help management make informed decisions. Be prepared to adjust and adapt new strategies as needed with changing circumstances.

For business owners, potential buyers, and sellers understanding working capital and the working capital requirement is more than just a financial exercise—it’s about ensuring the heartbeat of the business.

The SBA SOP 50 10 (7).1 require a business valuation for SBA Loans that include $250,000 or more in intangible assets. In addition, a business valuation is required on all closely related party transactions regardless of the dollar amount of the intangible assets. A closely related party is a family member, long time employee, etc.

The requirements for a valuation state that it must be provided by a qualified source. The list of qualified sources include valuation analysts who are certified valuation analyst and accredited senior appraisers. One important distinction between valuation analysts is whether they are Certified Public Accountants “CPA” too. The CPA license provides assurance that the valuator understands complicated accounting and tax issues.

Whether you are thinking about buying or selling a business. Understanding the intricacies of SBA SOP 50 10 (7).1 including the valuation provision is helpful to ensure your deal will be successful.

Understanding what EBITDA represents is critical to understanding the value of a business. The acronym stands for earnings before interest, taxes, depreciation and amortization. This metric, which is synonymous with cash flow was coined in the 1970s by Billionaire John Malone. The importance of cash flow in business valuation cannot be overstated. While real estate valuation is often dependent on location, location, location, business valuation is dependent upon cash flow, cash flow, cash flow. If a business has a healthy cash flow it will be worth more than its tangible assets. If cash flow is paltry or if the business is a holding company, then it is likely worth only its tangible asset value minus its liabilities (where assets and liabilities are adjusted to fair market value).

The calculation of historic EBITDA is straightforward. Start with net income before taxes then add interest, depreciation, and amortization. This information can be obtained from the business tax returns or financial statements. Often historic EBITDA must be adjusted to account for certain expenses from the Profit and Loss that are non-recurring or non-operational. These adjustments provide the owner with the cash flow stream adjusted to economic reality which is the benefit stream that can be sold or enjoyed by the owner. Some folks call these adjustments “addbacks.” In business valuation parlance they are referred to as normalizing adjustments as the valuation analyst normalizes the cash flow stream to depict economic reality.

The adjusted EBITDA is the metric most often used by parties to mergers & acquisitions. Businesses often sell for a multiple of normalized EBITDA. More than any other measure EBITDA is the catalyst that drives the value of a business. This is intuitive. If an investor can buy $5MM in cash flow for $25MM it is a better deal than buying a similar business with $4MM in cash flow for $26MM. Likewise the more cash flow or EBITDA a seller has to sale the more the business is worth.

Perhaps you have heard the terms P&L and balance sheet before, but you are not quite sure what they tell us about a business. In this article we provide you with analogies that will help you understand the three parts of the financial statements. We begin with Profit and Loss. This report provides the user with details on how much revenue and expenses were recognized during a period of time. If the revenues are greater than the expenses the business has net income.

The Balance Sheet is the second part of the financial statements we tackle. Whereas the Profit and Loss depicts the revenues and expenses the Balance Sheet shows the assets, liabilities, and equity balances of the business as of a specific date. This report provides users with the overall position of the business with regards to the assets it owns versus the liabilities it owes. The difference between the assets minus the liabilities is the equity.

The statement of cash flows is the third part of the financial statements we discuss. This statement provides the user with a detailed glimpse of the change in cash over a specific period. This statement is critical for management due to the importance of maintaining enough cash but not too much. It can help management avoid a cash flow crunch and identify whether the company is accumulating cash or depleting cash.

Business valuators and other folks typically include the market approach to ascertain the value of a business. The approach tends to be the most intuitive and easy to understand. But users of the comparable sales databases often encounter the inclusion of distressed sales and synergistic sales in the database. Unlike most transaction databases the Peercomps database excludes distressed sales or transactions at the investment (synergistic) level of trade. This is very helpful when the preparer of the valuation desires to the know the fair market value of the target business.

The Peercomps database consists solely of SBA transactions and the SOP 50 10 (7) .1 which governs the SBA program do not allow the lenders to loan for the purchase of a distressed business neither does the SOP allow for a buyer to purchase a business for greater than fair market value. This peer reviewed article discusses the advantages of using the Peercomps database. It also sheds light on which assets are included in the market value of invested capital for each transaction.

This peer reviewed article discusses the highly debated topic regarding whether a controlling interest in private equity can suffer from a discount for marketability. It is well documented that minority interests of private equity can suffer from a lack of marketability. The studies valuators rely upon to quantify the discounts for marketability for minority depict that the discount can range anywhere from 13%-72%. But there are no empirical studies to measure any lack of marketability for control interests of less than one hundred percent.

The solution provided in the article to quantify whether a discount for lack of marketability exists is based upon the internal rate of return calculated for the hypothetical buyer of a minority interest. An example with assumptions is provided to demonstrate the usefulness of this methodology. Using the IRR function in excel the author calculates the IRR for a hypothetical buyer of a 51% interest in a Heating Ventilation and Air Conditioning business. The methodology employed in this article provides the valuation community, attorneys, bankers, business brokers, and others with a quantifiable means to ascertain if a discount for marketability exists for a controlling interest of less than one hundred percent.

Machinery & equipment appraisers are often asked to value equipment at different levels of trade e.g., value installed, value in continued use, orderly liquidation value, etc. For example, a bank may need to know the liquidation value of equipment in the event they have to foreclosure on the business. Understanding and applying the correct standard of value and level of trade is required by the Uniform Standards of Professional Appraisal Practice. But what happens when an equipment appraiser uses an incorrect standard of value and an incorrect level of trade to value machinery & equipment? The answer is it creates chaos for the end user.

In this article the author details how to discern the level of trade comparable sales or comparable ‘for sale’ assets are traded at. This article stems from the author’s personal experience working on behalf of Mecklenburg County, North Carolina to thwart a business personal property tax appeal made by a large North Carolina based company. The opposing appraiser hired by the company used ‘for sale’ assets identified on auction sites, e-bay, etc. to estimate the value of installed equipment. The author used ‘for sale’ assets held at the fair market value level of trade. The deficiencies in the method used by the company’s appraiser included not accounting for installation, shipping, assembly, disassembly, effective age, condition, etc. The Court of Appeals and Supreme Courts of North Carolina ultimately upheld the County’s appraisal and refuted the appraisal made on behalf of the company.

Ready to Discuss Your Business Valuation?

Connect with us Today for a Personalized Consultation

FREE Sample Appraisal Report

Do you want to know what your equipment is really worth? Are you wondering if your business could benefit from getting a business valuation? If so, you have come to the right place!

FREE Sample Appraisal Report

Do you want to know what your equipment is really worth? Are you wondering if your business could benefit from getting a business valuation? If so, you have come to the right place!

Business Valuations and Machinery & Equipment Appraisals in Charlotte NC

Industry Insights

- Copyright © 2023 Turner Business Appraisers

- Site Design by Deal Studio